Crypto Payments vs SWIFT: What Businesses Should Choose in 2026

May 18, 2026

5 min read

Contents

What is SWIFT and How Does It Work?

Key Problems of SWIFT for International Payments

What Are Crypto Payments and How Do They Work?

Crypto as a SWIFT Alternative

Crypto Payments vs SWIFT: Full Comparison

When SWIFT Still Makes Sense

How Businesses Use Crypto for Cross-Border Payments

Compliance and Security Considerations

How Inqud Enables Global Crypto Payments

Share

The world of global trade is massive. By the end of 2026, experts expect cross-border payment volumes to hit roughly $250 trillion. That is a staggering amount of capital moving across borders every single day. Even so, many companies still rely on systems built in the 1970s. We see businesses losing about 2% to 5% of their transaction value just to hidden fees and currency exchange spreads. It is a real headache for growth.

Deciding how to move your company funds is a big deal. You have the old reliable SWIFT network on one side. On the other side, you have the digital asset world. Both have their place. But the gap in efficiency is getting harder to ignore. If you are thinking about accepting crypto payments, you are looking at a system that never sleeps. Traditional banks do sleep. They close on weekends and holidays.

At Inqud, our team works with these challenges daily. We wrote this guide because we want to share our expertise. We would be glad to assist you with a crypto payment gateway to make these processes smoother.

Most integration questions we get start right here — get in touch with our team and we'll go through crypto payments vs SWIFT against your actual stack.

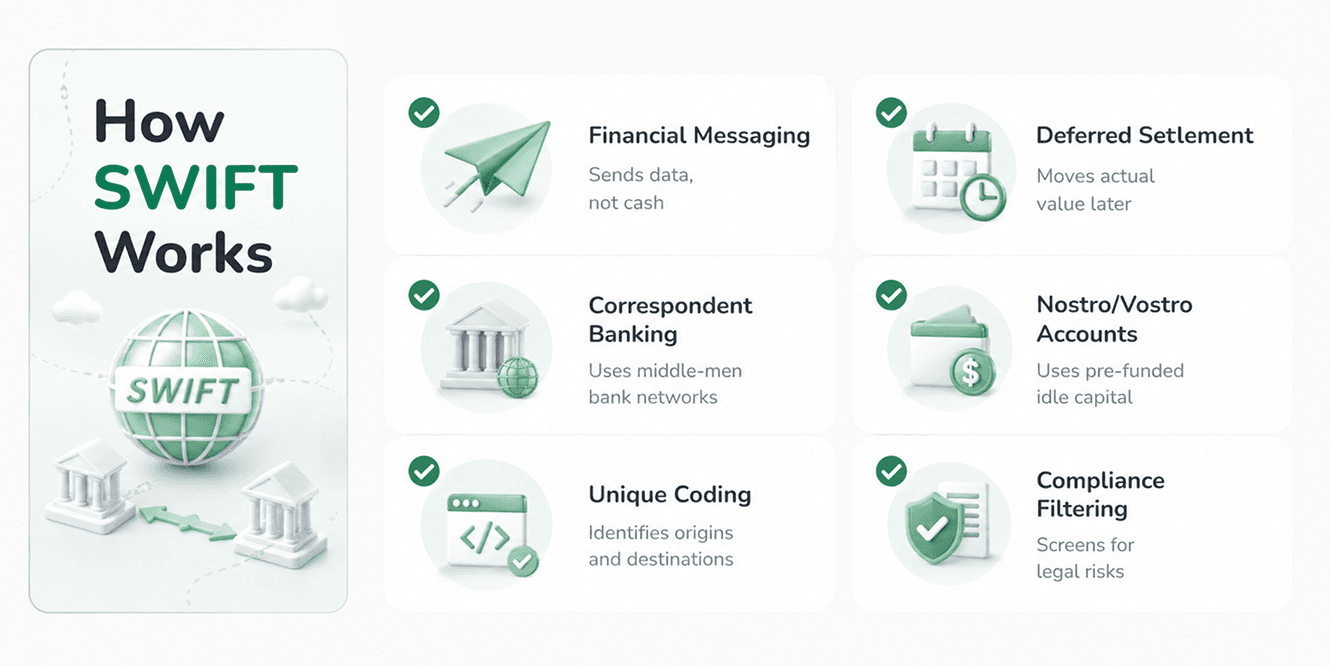

What is SWIFT and How Does It Work?

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. It is not actually a bank. We can compare it to a very secure, very old social network for banks. When you send a wire, you are not sending actual cash through a pipe. You are sending a message. That message tells one bank to debit an account and another to credit one. It is a system built on trust and a long chain of partners.

|

Feature |

Description |

|

Established |

1973 |

|

Reach |

11,000+ institutions |

|

Daily Volume |

Over $5 trillion |

|

Core Function |

Financial messaging |

The Correspondent Banking System

Most banks do not have a direct connection to every other bank in the world. So, they use "correspondent banks" as middle-men. If you send money from a small bank in Italy to a small bank in Vietnam, the money might pass through three or four other banks in between. Each one of these stops adds a bit of time and a bit of cost.

SWIFT Messaging and Settlement

When you start a transfer, a SWIFT message is sent using a specific code. This code tells the receiving bank where the money is coming from and where it should go. The settlement (the actual movement of value) often happens later through a clearing house. This separation of the message and the money is why things feel so slow.

Why SWIFT Transfers Take Time

Time is the biggest enemy here. Because of the different time zones and different bank working hours, a message might sit on a desk for twelve hours before anyone looks at it. Then the next bank in the chain does the same. This is a primary reason why people look for a SWIFT alternative crypto solution.

The Role of Nostro and Vostro Accounts

Banks keep money in each other's accounts to make these transfers work. These are called Nostro and Vostro accounts. It requires banks to keep billions of dollars just sitting idle in accounts all over the world. It is a very capital-inefficient way to run a global economy.

Compliance and Manual Reviews

Every single international wire goes through a series of filters. These check for money laundering risks and sanctions. Often, a perfectly legal payment gets "flagged" because a name looks similar to someone on a list. A human then has to manually check it. This adds days to the process.

Centralized Infrastructure Governance

SWIFT is owned by its member banks. While this makes it stable, it also makes it very slow to change. Upgrading the system takes decades because everyone has to agree on the new rules. This lack of agility is why modern fintech is starting to pull ahead.

Key Problems of SWIFT for International Payments

Even though it is the global standard, SWIFT has some deep flaws. For a modern business, these flaws represent lost opportunities. If your money is stuck in transit for five days, you cannot use it to buy inventory or pay staff.

|

Problem |

Impact on Business |

|

Speed |

1–5 business days delay |

|

Cost |

3%–7% total loss in many cases |

|

Visibility |

"Black hole" effect during transit |

|

Reliability |

4%–10% error or inquiry rate |

High and Non-Transparent Fees

You rarely know exactly how much money will arrive at the destination. The sending bank charges a fee. The intermediary banks take a "toll." The receiving bank might charge a landing fee. By the time the money hits the account, it is often much less than you expected. Using a crypto payment widget usually removes these surprises.

Slow Settlement Times

We live in a world of instant messages and instant shipping, but money moves like it is still 1950. Waiting a week for a payment to clear is simply not acceptable for many fast-moving startups. This friction slows down the whole global supply chain.

Limited Availability

Banks close. They close at 5 PM. They close on Saturdays. They close for bank holidays. If you need to settle a contract on a Friday evening, you are out of luck until Monday or Tuesday. This is a huge contrast to international payments crypto systems which run 24/7/365.

Data Truncation and Loss

The old SWIFT messaging format has limited space for information. Sometimes, the reference note you attached to a payment gets cut off. When the money arrives, the accounting department has no idea which invoice it is for. This leads to hours of manual reconciliation.

High Rejection Rates

Errors happen often. A wrong IBAN or a slightly misspelled bank name can cause the whole payment to bounce. But it doesn't bounce instantly. You might wait four days only to find out the money is coming back to you, minus the fees.

Lack of Real-Time Tracking

Historically, once you sent a wire, it disappeared into a "black hole." You couldn't see where it was. While SWIFT gpi has improved this, not all banks use it. Many businesses are still left wondering where their millions of dollars are currently sitting.

If you're paying $25–50 per wire plus FX spread on top — talk to us about your cross-border corridors. We'll build a custom comparison of your SWIFT cost vs. a stablecoin setup for your volumes and destinations. 4-hour reply.

Tip: Check the Corridor

Before sending a large wire, ask your bank if they have a direct relationship with the destination. If they don't, expect at least two intermediary banks to take a cut of your funds.

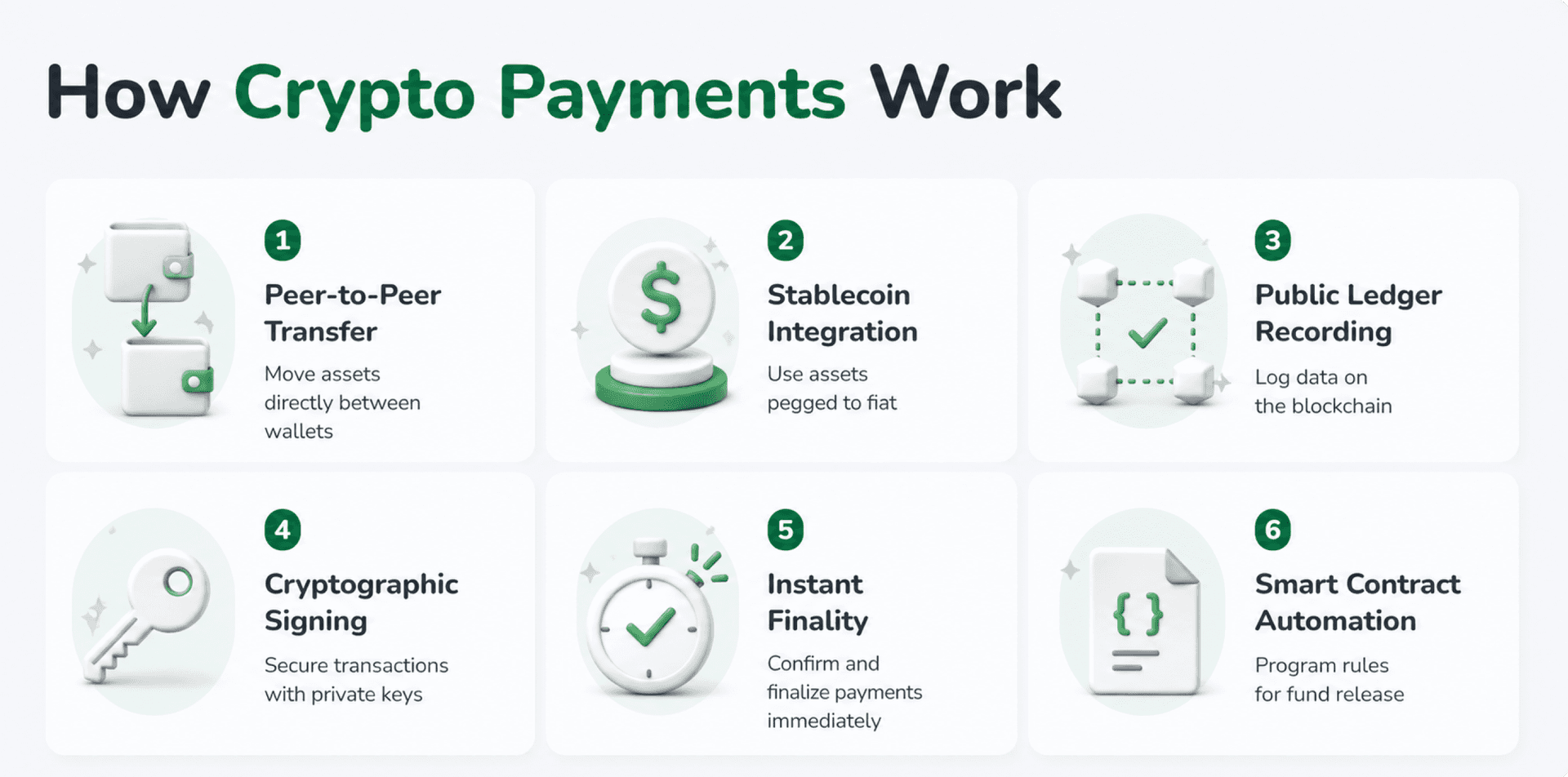

What Are Crypto Payments and How Do They Work?

At its heart, a crypto payment is just a line of code on a shared ledger. There is no "message" separate from the "money." The message is the money. When you use a SWIFT alternative crypto method, you are moving digital assets directly from your wallet to another.

Direct Peer-to-Peer Transactions

There is no middleman bank in a blockchain transaction. You send the value directly to the recipient. This removes the "toll booths" we talked about earlier. It makes crypto payments vs SWIFT a very different experience because you are in control of the timing.

Stablecoins for Price Stability

Most businesses do not want to use volatile assets like Bitcoin for payroll. Stablecoins like USDT or USDC are pegged 1:1 to the US Dollar. You get the speed of blockchain with the price stability of traditional currency.

Public Ledger Transparency

Every transaction is recorded on a public blockchain. Anyone with the transaction ID can see that the money was sent and that it arrived. You don't have to call a bank to ask for a status update. The data is right there for everyone to see.

Cryptographic Security

Instead of relying on a bank's internal security, these payments use advanced math. Each transaction is signed with a private key. It is nearly impossible to forge. This level of security is why many firms now choose recurring payments via blockchain.

Instant Finality

In many modern blockchains, once a transaction is confirmed, it is final. There is no "pending" state that lasts for days. This allows businesses to release goods or services immediately after the payment is detected on the network.

Programmable Money

You can set up rules for your payments. For example, you can use a payment link that only releases funds once certain conditions are met. This is something traditional wire transfers simply cannot do without a very expensive escrow service.

Crypto as a SWIFT Alternative

Comparing these two is like comparing a horse and carriage to a jet engine. One is a legacy of the past, and the other is the future. For a global business, the benefits of moving to a SWIFT alternative crypto model are clear and immediate.

|

Benefit |

Why it matters |

|

Speed |

Minutes vs Days |

|

Fees |

Often less than $1 regardless of amount |

|

Access |

Anyone with internet can participate |

|

Uptime |

Never closes |

Faster Cross-Border Transactions

The biggest of benefits of accepting crypto is speed. A transaction from New York to Singapore takes the same amount of time as a transaction to your neighbor. Usually, this is under ten minutes. When we look at crypto payments vs SWIFT, the time savings alone can save a business thousands in liquidity costs.

Lower Fees and Predictable Costs

Blockchain fees are usually based on network traffic, not the amount of money you send. Sending $1 million costs the same as sending $100. This is a game changer for high-value B2B transactions. It makes your financial planning much more accurate.

24/7 Global Availability

The blockchain doesn't care about Christmas or bank holidays. It doesn't care if it is 3 AM. If you need to move money, you move it. This 24/7 nature allows for "just-in-time" payments, which keeps your capital working for you longer.

Transparency and Traceability

You can prove you paid a supplier instantly. You just send them the link to the block explorer. No more "the check is in the mail" excuses. This builds trust between partners, especially in international payments crypto scenarios where parties might not know each other well.

Permissionless Innovation

You don't need to ask a bank for permission to open an account or send a payment. As long as you follow the rules of the protocol, the network serves you. This is vital for businesses in regions where the traditional banking system is poorly developed or overly restrictive.

Simplified Accounting

Digital payments often come with better data. You can attach detailed metadata to a blockchain transaction. This makes it easier for your software to categorize the expense automatically. Your bookkeeping becomes much less of a chore.

Tip: Watch the Gas

Network fees (gas) can spike during busy times. If your payment isn't urgent, wait a few hours. You might save 50% on the transaction cost by just picking a quieter time of day.

Crypto Payments vs SWIFT: Full Comparison

When we put them side-by-side, the differences are stark. It really comes down to what your business prioritizes. If you value old-school institutional backing, SWIFT is there. If you value efficiency and modern tech, crypto wins.

|

Feature |

SWIFT |

Crypto (Stablecoins) |

|

Settlement Speed |

1 to 5 days |

Seconds to minutes |

|

Operating Hours |

Banking hours only |

24/7/365 |

|

Cost Structure |

Percentage based + flat fees |

Network fee (usually flat/low) |

|

Intermediaries |

Multiple banks involved |

None (Peer-to-peer) |

|

Transparency |

Low (Internal bank systems) |

High (Public ledger) |

|

Failure Rate |

Moderate (Manual errors) |

Very Low (Protocol based) |

|

Regulatory Status |

Fully regulated |

Varies by jurisdiction |

|

Ease of Use |

High (Integrated in banks) |

Improving (Requires a gateway) |

The reality is that crypto payments vs SWIFT is becoming less of a debate and more of a transition. Companies are realizing that they don't have to settle for the "slow lane" anymore.

The table above is generic. Send us your transaction data — volumes, corridors, current fees — and we'll build a personalized breakdown showing exactly where crypto rails beat SWIFT for your business. 25-min call, 4-hour reply.

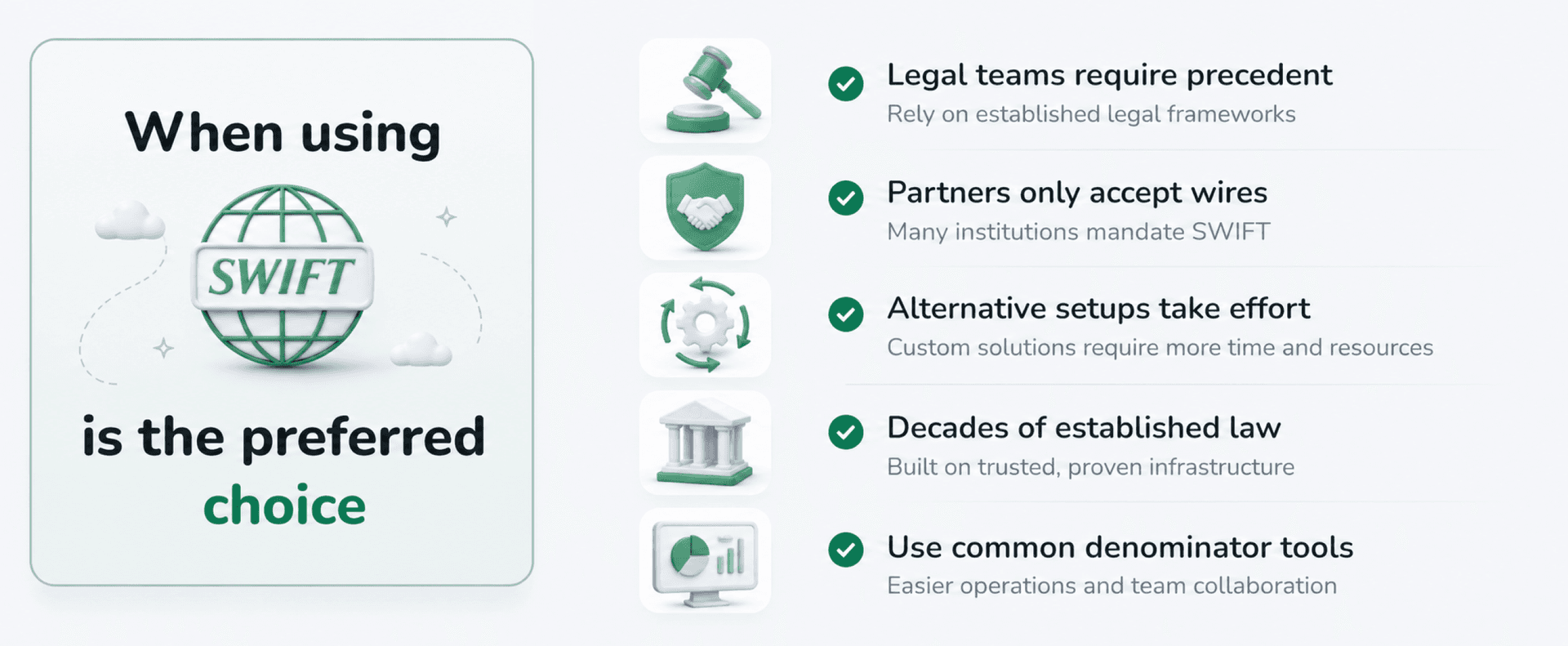

When SWIFT Still Makes Sense

We have to be realistic, the traditional system isn't dead yet. There are times when using a bank wire is actually the better choice. It is about choosing the right tool for the job.

Consider the regulatory environment

If you are a massive corporation with very strict compliance mandates, your legal team might insist on using SWIFT. The traditional banking system has fifty years of legal precedent behind it. That gives some executives a sense of security that code cannot yet provide.

Think about your partners

If your supplier in a remote region doesn't know how to use a digital wallet, you can't pay them in crypto. You are limited by what the other person can receive. Until everyone adopts these tools, the bank wire remains the "lowest common denominator" for global trade.

Look at the size of the transaction relative to the complexity

For a very small business that only does one international transfer a year, the effort to set up a SWIFT alternative crypto workflow might not be worth it. Sometimes, the familiar path is the easiest, even if it is more expensive.

How Businesses Use Crypto for Cross-Border Payments

Many firms are getting creative with how they use these assets. It is basically about rethinking how a treasury works.

Handling large volumes

Many companies now use an OTC desk to handle large volume conversions. They might move $5 million in USDC across the world in minutes, then convert it to local currency on the other side. This avoids the volatility of the market while keeping the speed of the blockchain.

Convenience for remote teams

If you have employees in five different countries, paying them through traditional banks is a nightmare. The fees eat up their salary. By using international payments crypto methods, you can pay everyone instantly. They receive the full amount, and you only pay one tiny fee.

High-frequency micro-payments

Imagine a software company that needs to pay hundreds of affiliates every day. Doing that via SWIFT would be impossible due to the minimum fees. With blockchain, it is easy and cheap.

Compliance and Security Considerations

Safety is a top priority. You cannot just send money into the void and hope for the best. When you accept crypto payments, you need to think about taxes and anti-money laundering (AML) rules.

Actually, blockchain is often more transparent than banking. Regulators can see every transaction. If you use a reputable provider, they will handle the KYC (Know Your Customer) checks for you. This means you get all the benefits of the tech without the legal headache.

Security is also about how you store your keys. You should never keep all your funds on a single exchange. Using multi-signature wallets is a smart move. It means three different people in your company have to approve a large payment before it goes out. This prevents fraud and internal theft.

Lastly, make sure you are keeping good records. Just because the money moves on a ledger doesn't mean the tax man doesn't want to see it. Most good crypto payment gateway services will provide you with clear reports that your accountant will love.

Tip: Use a Professional Gateway

Don't try to manage business crypto on a personal phone app. Use a professional service that offers roles, permissions, and audit logs. It is much safer for your company's treasury.

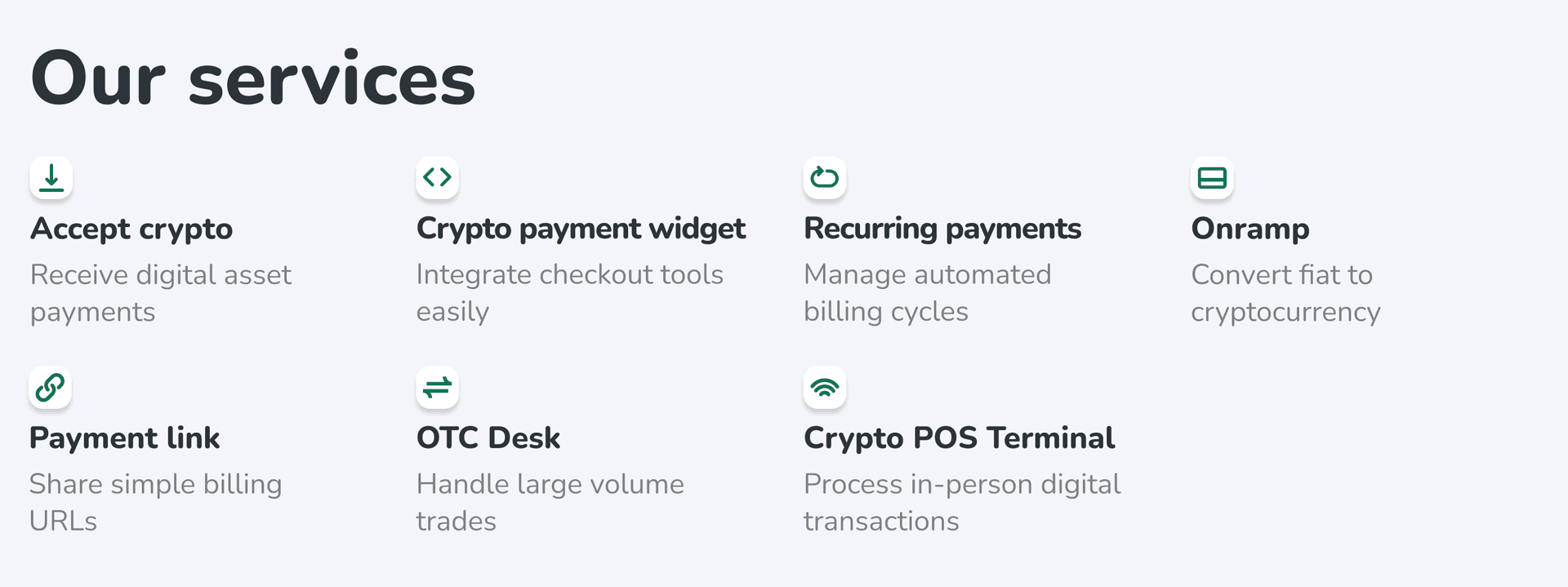

How Inqud Enables Global Crypto Payments

In the end, the choice between crypto payments vs SWIFT comes down to your need for speed and cost-effectiveness. That is why we built our platform – we wanted to take the complexity of the blockchain and turn it into something a regular business can use. Our goal is to make international payments crypto as easy as sending an email.

Whether you need a crypto POS terminal for a physical store or a complex API for an online shop, we have the tools. We focus on security and ease of use. You don't need to be a blockchain expert to save money on your transfers. Our team handles the technical heavy lifting so you can focus on growing your business.

Sandbox keys within 1 business day. Send us your corridors and volume, and we'll come back with a live setup map, fee breakdown, and test environment to validate before you commit. 4 business hours to first reply.

We provide a robust crypto payment gateway that integrates directly with your existing systems. You can receive payments in digital assets and have them settled in your local currency if you prefer. This gives you the best of both worlds. We are proud of the expertise we have built up over the years.

If you are ready to stop waiting on slow bank wires, our team will be glad to help you make the right choice for your future.

Industries

Web3 payments

Products

OTC desk, API, Crypto widget, Сrypto payment gateway, Сard2crypto

Tags

Payment methods, Educational

Author

FAQ

FAQ

Is crypto a real alternative to SWIFT?

Yes, it is already being used by thousands of companies to move billions of dollars every month with much higher efficiency.

Are crypto payments cheaper than SWIFT?

Usually, they are significantly cheaper because they bypass the multiple intermediary banks that each take a fee.

How fast are crypto international payments?

Most transactions settle in minutes, which is a massive improvement over the several days traditional wires often take.

Are crypto payments safe for businesses?

When you use a professional service and follow basic security rules, they are actually more secure and transparent than old banking systems.

Can crypto replace traditional banking systems?

While they might not replace banks entirely, they are definitely replacing the plumbing of how money moves across borders.

Inqud Solutions for Your Business

Digital Currency Payments

Start accepting cryptocurrency payments from customers worldwide

Crypto Payment Widget

Embed a cryptocurrency payment widget on your website

Auto Billing

Set up automatic subscription and recurring billing in crypto

Payment URL

Create and share payment links for crypto transactions

Crypto Purchase Gateway

Enable users to buy crypto with fiat currency seamlessly